📅 On June 10, 2025, a regular lesson was held within the framework of the international virtual mobility program “Econometrics”, implemented by Sumy State University and Mahatma Jyotiba Phule Rohilkhand University (MJPRU, Bareilly, India).

🌐 The Econometrics program continues to unite students and professors from different countries around topical issues of economics, statistics and analytics. This time the topic of the meeting was “GARCH models using EViews”. The lecturer of the class was Dr. Ayben Koy, a professor at Istanbul Ticaret University (Turkey).

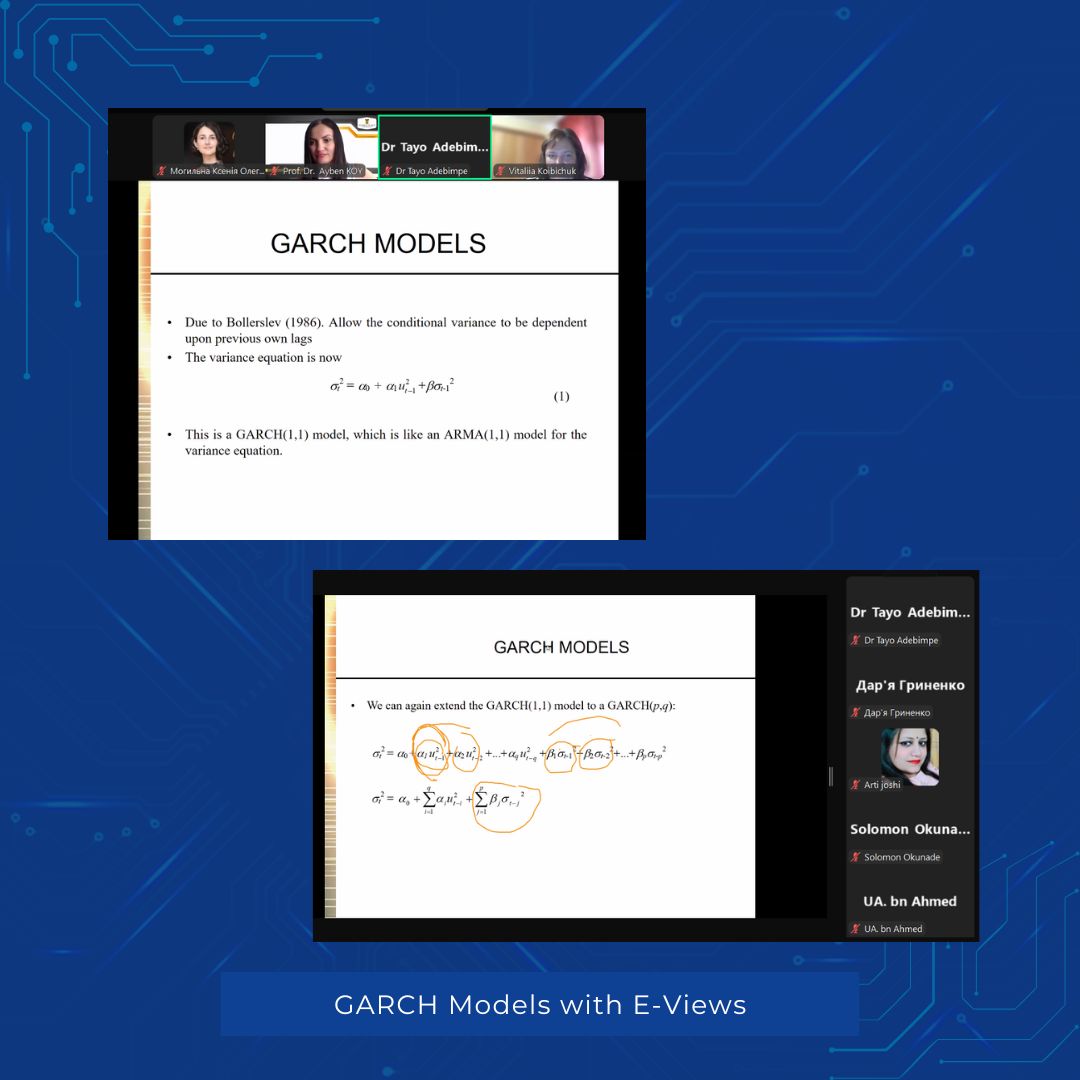

👩🏫 In her lecture, Dr. Ayben Koy introduced the participants to the theoretical foundations and practical aspects of applying GARCH models in financial analysis, in particular for predicting asset volatility.

🔍 During the lecture, the participants considered:

🔹 the basics of GARCH models and their variations (EGARCH, GJR-GARCH);

🔹 analysis of market data on the example of Turkish Airlines shares;

🔹 the importance of using logarithmic transformations to achieve stationarity of time series;

🔹 practical tips on choosing an ARMA structure using EViews;

🔹 comparison of classical models with modern approaches: TVP-SVM, neural networks, stochastic volatility models.

✨ We thank all participants for their active participation, interesting questions, and additions. We are looking forward to the next classes to continue to deepen our knowledge of econometrics and share international experience!

{kind=link}

{kind=link}

{kind=link}